Car Insurance Groups Explained: A Parent's Guide (2026)

Quick answer

A car insurance group is a 1-50 rating that tells insurers how risky a car is to cover. Lower numbers usually mean cheaper premiums. For 17 year olds, Group 1 is rarely the cheapest in practice.

The “popularity paradox” means cars in Groups 5-12 (like the Fiat 500 or Hyundai i20) often return lower real-world quotes for 17 year olds than Group 1 cars. Their claims pool is less concentrated with inexperienced drivers, so insurers price them more keenly.

What is an insurance group?

A car insurance group is a rating from 1 to 50 that tells insurers how risky a car is to cover. Group 1 is the lowest risk and usually the cheapest to insure. Group 50 is the highest risk and the most expensive. The rating is set by Thatcham Research and reviewed by a panel of UK insurers.

For cars launched after August 2024, the system is being replaced by the Vehicle Risk Rating (VRR), which scores each car from 1 to 99 across five separate pillars instead of a single number.

The UK insurance group system is a collaboration between Thatcham Research (the UK's only independent automotive risk intelligence organisation) and the Association of British Insurers (ABI). Thatcham maintains a proprietary database called Plaza, which receives technical data directly from car manufacturers. The data is analysed by the Group Rating Panel, made up of representatives from the ABI and Lloyd's Market Association.

"Since 2012 vehicles with standard fit AEB (Autonomous Emergency Braking) systems... have seen a reduction in their vehicle grouping, translating into potential savings of around 10% on consumers' insurance premiums."

The panel evaluates 125 vehicle attributes across six key factors:

- New car value: Higher value cars cost more to replace in a total loss scenario, pushing them into higher groups.

- Parts pricing: Thatcham compares the cost of 23 common repair components. Cheaper parts correlate with lower group ratings.

- Repair times: Complex designs requiring more labour hours increase the rating. Longer repair times mean higher claim costs.

- Performance: Acceleration times (0-60 mph), top speed and weight are evaluated. High performance is statistically linked to more frequent and severe accidents.

- AEB fitment: Standard fit Autonomous Emergency Braking systems can lower a car's rating by reducing the likelihood of front to rear collisions.

- Security: The effectiveness of immobilisers, alarms and door locks is reflected in a security suffix (more on this below).

In the traditional 1-50 system, which still applies to all cars launched before August 1, 2024, the panel assigns an advisory group rating. The rating is not mandatory. Individual insurers are free to adjust their pricing based on their own claims data, which is why quotes for the same Group 5 car can vary wildly between providers.

Understanding security suffixes

Every traditional group rating includes a letter suffix:

- A (Acceptable): Meets security standards for the assigned group

- E (Exceeds): Security is superior. The car is often moved to a lower group (e.g. 9 to 8E)

- D (Does Not Meet): Security falls short. The car is moved to a higher group (e.g. 9 to 10D)

- P (Provisional): Rating is incomplete at the time of launch

- U (Unacceptable): Security is well below standards. Insurers may refuse cover without an alarm upgrade

- G (Import): The car is a non-UK specification import and cannot be rated under standard rules

The 2026 shift: Vehicle Risk Rating (VRR)

As of 2026, the industry is midway through an 18 month transition toward the Vehicle Risk Rating (VRR) model. The shift was driven by the move from mechanical-heavy car designs to "software-defined cars" and the rapid growth of EVs. The VRR system, which applies to all new model ranges registered from August 1, 2024, moves from a single static rating to a dynamic score across five assessment "pillars":

- Performance: Evaluates acceleration, top speed, list price and the impact of modern drivetrains (EV and Hybrid) and their unique insurance risks, such as high torque delivery

- Damageability: Uses rigorous testing to determine how a car's design, materials (like aluminium or carbon fiber) and construction techniques affect the severity of damage in typical collisions

- Repairability: The most influential pillar for premiums. It analyses the ease of repair, encourages manufacturers to provide transparent repair strategies and prioritises accessible parts. Repair costs rose 28% in 2024, making this a top priority for insurers

- Safety: Beyond crash tests, this analyses active safety systems (crash avoidance) and physical attributes like kerb weight

- Security: Stems from the New Vehicle Security Assessment (NVSA). It looks at physical anti-theft devices and, for the first time, digital security and cybersecurity against remote hacking

Each pillar is scored from 1 to 99, with 1 representing the lowest risk. This allows insurers to see why a car is risky. For example, a car might be highly safe but incredibly expensive to repair.

For parents, the takeaway is that a car launched after late 2024 will not have a "Group 5" rating, but rather a "VRR" score. A low VRR across all five pillars is the new gold standard for affordable insurance.

"The VRR (Vehicle Risk Rating) represents a fundamental shift... [it] will not only help insurers price premiums more accurately but also encourage manufacturers to consider insurance outcomes when designing vehicles."

Why 17 year olds pay £1,932 a year

The statistics of first year risk

Young driver insurance is expensive because the risk is real and measured. According to Brake and the ABI, one in five new drivers crashes within the first twelve months of passing their test.

Drivers under 20 are 33% more likely to be in a road accident than drivers in their 40s or 50s, and those crashes tend to be more severe. Insurers use the group system to manage that risk. By steering young drivers toward lower-group cars (smaller engines, better safety tech), the industry tries to limit the potential speed and force of those early collisions.

"17 and 18 year old car insurance is about more than just age. Insurers look at your postcode, the car you drive, whether it's parked off-road and how much you drive each year."

Financial realities in 2026

The average UK annual premium has settled at around £607. The story for 17 year olds is different. In 2026, the average comprehensive policy for a 17 year old is £1,932. That's much lower than the £3,000+ quotes seen in early 2024, but it's still the highest cost of any age bracket.

Choosing a lower-group car isn't a preference. It's a financial necessity for most families. Picking a Group 1 car over a Group 10 car can save a 17 year old more than £1,000 in their first year alone.

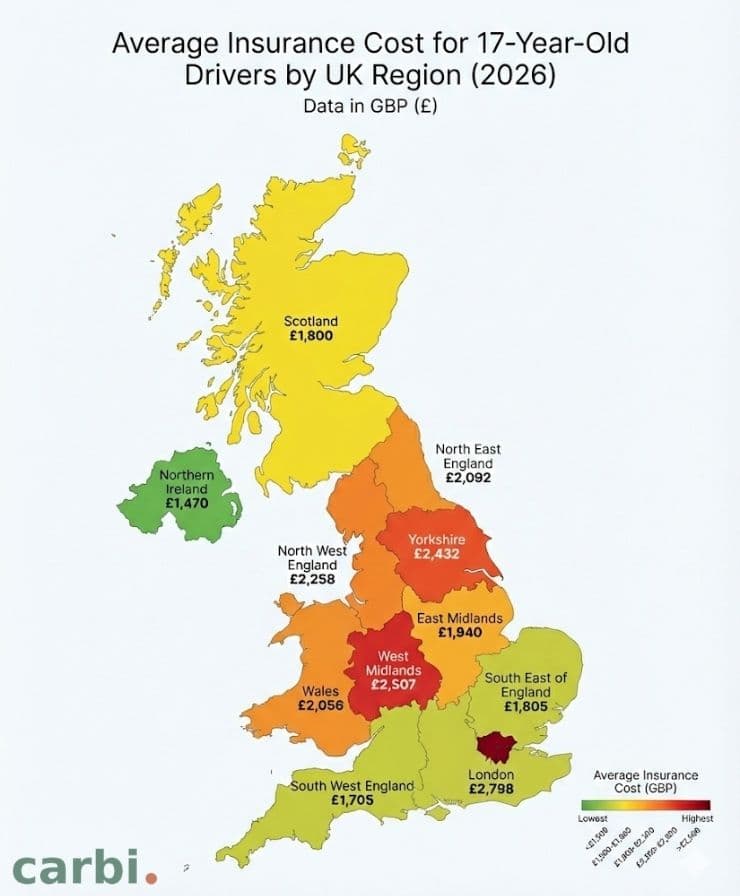

Regional Considerations

Where you live changes what car you should buy.

| Region | Avg. 17yo Premium | Consideration |

|---|---|---|

| Northern Ireland | £1,470 | Reforms planned this year for 24 month R-plates and nighttime passenger restrictions for under-24s. |

| South West | £1,705 | Lowest National Premiums |

| Scotland | £1,800 | Aberdeen is the UK's cheapest city for insurance, but rural young drivers face higher costs due to higher annual mileage. |

| East of England | £1,805 | Higher rural mileage offsets lower urban crime rates. |

| East Midlands | £1,940 | Near the national average for teenage risk. |

| Wales | £2,056 | Impacted by 20mph limits and rural road severity. |

| North West England | £2,092 | Specific postcode vulnerabilities in NE and SR areas. |

| Yorkshire | £2,432 | High claims frequency in Leeds and Sheffield hubs. |

| West Midlands | £2,507 | Elevated collision rates in urban Birmingham/Coventry. |

| London | £2,798 | Highest density of theft and ULEZ-related costs. |

If you live in a high premium area like London or Manchester, choosing a car from the absolute lowest insurance groups (1-3) becomes even more critical to keep the total bill under the £2,500 mark.

Insurance groups for popular first cars

Looking up a specific model? We've built dedicated insurance-group pages for the cars parents ask about most often, with the indicative 17 year old premium for each.

Don't see your model? Use the Groups 5-12 framework below to estimate where your car sits from its trim and engine.

Why Groups 5-12 beat Group 1 for most 17 year olds

Groups 5 to 12 are the band where the popularity paradox flips. Cars in this zone are slightly larger, better equipped, and less concentrated in the teenage claims pool than Group 1 city cars. For most 17 year olds, a Groups 5-12 car returns a lower real-world quote than a Group 1 alternative, despite sitting higher on the group scale.

What does each group cost a 17 year old?

The insurance group predicts relative cost. The real quote a 17 year old sees depends on postcode, telematics, and named-driver structure. These are the indicative annual premium ranges Carbi sees most often for a new driver on a comprehensive policy in 2026.

"At 17, your car insurance is always going to be expensive. Being realistic about choosing a car you can afford to insure will go a long way to making your insurance affordable."

| Insurance group | Low | Median | High | Notes |

|---|---|---|---|---|

| Group 1 | £1,400 | £1,750 | £2,200 | Citigo, Up, Panda. Popularity paradox often pushes quotes higher than Group 5 |

| Group 5 | £1,500 | £1,850 | £2,350 | Cheap-band entry. Fiat 500, Hyundai i10 |

| Group 10 | £1,650 | £2,000 | £2,600 | Cheap-band exit. Hyundai i20, Polo upper trims |

| Group 15 | £1,900 | £2,400 | £3,200 | Just above the cheap band. Fabia upper trims |

| Group 20 | £2,300 | £2,950 | £4,000 | Performance trims, larger superminis |

| Group 30 | £2,800 | £3,800 | £5,500 | Group warning territory. Audi A1, BMW 1 Series |

| Group 40 | £3,500 | £4,800 | £7,000 | Avoid for first car |

| Group 50 | £4,500 | £6,500 | £9,500+ | Off-strategy for new drivers |

Why groups 1-3 aren't always cheapest

The standard advice for parents is to buy a Group 1 car. Group 1 cars (Volkswagen up!, Skoda Citigo, certain Fiat Pandas) are inherently cheap to insure thanks to low performance and cheap parts, but they are not always the real-world price leaders. For a wider look at which cars are cheap to insure across every budget, see our main first car guide.

The reason is the popularity paradox. Group 1 cars are so common among new drivers that the claims pool for those specific models is filled with accidents caused by teenagers. Insurers price from their own data. If 1,000 teenagers crash a Group 1 Citroen C1 but only 100 teenagers crash a Group 5 Fiat 500, the Fiat 500 will often return lower quotes for a 17 year old.

Why Groups 5-12 win

For many 17 year olds in 2026, the cheap-to-insure band lies in Groups 5 to 12. Cars in this band are often slightly larger, more robust, and better equipped with safety features than the bare-bones entry-level Group 1 city cars.

Real-world data from the RAC and quote comparison sites often shows the Fiat 500 (typically Groups 5-10) is the cheapest car to insure for 17 year olds, despite not being in Group 1. The Hyundai i20 (Groups 5-12) often returns cheaper quotes for new drivers than the smaller, lower-grouped Hyundai i10. Many of these cars can be found for under £3,000.

| Model | Insurance Group | Why it works for 17 year olds |

|---|---|---|

| Fiat 500 · details | 5-10 | High desirability but stable claims history among new drivers |

| Peugeot 108 | 1-5 | Nearly identical to Aygo/C1 but often returns lower quotes |

| Hyundai i20 | 5-12 | Larger and more stable than the i10, appealing to a broader risk pool |

| Volkswagen Polo · details | 1-8 | High build quality and standard safety kit. Stable premiums |

| Skoda Fabia | 4-15 | Often cheaper to insure than its sister car, the VW Polo |

Insurance group vs premium costs

The takeaway for parents is that the insurance group predicts relative cost, not absolute cost. A Group 10 car will always be cheaper to insure than a Group 40 car for the same person in the same location. Within Groups 1 to 15, individual insurer preferences and claims data for your specific age and location will shuffle the rankings.

That's why running real quotes is essential. Don't just look at the group number on a listing. Run dummy quotes for several cars in the shortlist to see which one the insurer's algorithm favours for your child's specific profile.

Real-World Example

For a detailed breakdown of how insurance groups translate to real-world running costs for young drivers, our Ford Fiesta vs Vauxhall Corsa guide compares Group 2 against Group 6 across different regions.

Common insurance mistakes

The "fronting" trap

"Fronting" is insurance fraud, not a technicality.

The biggest legal error parents make is "Fronting." This is when a parent is listed as the "Main Driver" on a policy to lower the premium, even though the teenager is the main user of the car. Parents often see it as a clever workaround. Legally, it's insurance fraud.

"Adding an older, 'safer' driver, such as a parent or relative, will cut the cost of your insurance policy... [but] you must list the person who drives the car most as the main driver, otherwise you may be accused of 'fronting'."

For the full breakdown, including how insurers detect fronted policies, the legal alternatives, and worked examples, read our dedicated guide: What is fronting and why parents must never do it.

If there's an accident, insurers have specialised investigators who can work out who the main user was (checking school/work commutes, parking locations, etc.). If caught, the policy is voided, the claim is refused, and the parent can be prosecuted for fraud. After that, any household member trying to insure a car will struggle to get affordable cover.

The legal alternative: List the teenager as the Main Driver and add the parent as a "Named Driver." This can legitimately save between £100 and £150 per year, as it signals to the insurer that a more experienced driver will be behind the wheel for a portion of the mileage. We cover the full trade-offs in our named driver vs own policy guide.

The third party only (TPO) myth

Historically, Third Party Only insurance was the go-to for saving money. In 2026, this is rarely true. Comprehensive policies are now frequently cheaper than Third Party, Fire and Theft (TPFT) or TPO.

Insurers have found that drivers who choose the minimum legal cover (TPO) are statistically more likely to be involved in accidents. Consequently, they have raised the price of TPO to reflect this higher risk profile. For an average driver, a third party policy is now 73% more expensive than fully comprehensive cover. Parents should always check comprehensive quotes first.

Underestimating the automatic premium

Automatic cars are often easier to learn in, which is why parents push their teenagers toward them. The cost on insurance is steep.

- Gearbox complexity: Automatic gearboxes are more expensive to repair and replace than manual ones

- The "Automatic Licence" loading: If a teenager holds an automatic only licence, their premium is likely to be 56% higher than those with a manual licence. This is because insurers see automatic only drivers as statistically higher risk, with a 46% higher claim frequency

- Group jumping: The same model of car will often be in a higher insurance group if it has an automatic gearbox. For example, a manual Kia Picanto might be in Group 1, while an automatic version could be in Group 4

Ignoring small modifications

A "modification" in the eyes of an insurer is anything that differs from the car's factory specification. This includes tinted windows, aftermarket alloy wheels, or even stickers. For a new driver, even a minor aesthetic modification can cause a premium to jump by 5-10% or, in some cases, result in a refusal to provide cover entirely.

How to use this information when choosing a car

The three-step selection strategy

To help parents navigate the market efficiently, Carbi recommends a three-step approach to using insurance group data during the car-buying process.

Step 1: Scrutinise the trim and engine, not just the model

A Vauxhall Corsa can range from Group 1 to Group 34. The difference is almost always found in the engine displacement and the trim level name.

| Corsa Trim Level | Engine | Insurance Group |

|---|---|---|

| Expression | 1.0L | 1-2 |

| Life / Active | 1.2L | 2-5 |

| Energy / SE | 1.4L | 3-12 |

| SRi / Limited Edition | 1.2L Turbo | 10-13 |

| VXR / GSi | 1.6L Turbo | 20-34 |

Parents should steer toward "Expression," "Life," or "Active" trims to stay in Groups 1-12.

Step 2: Check for "safety packs"

When looking at newer used cars (2019 onwards), check if the original buyer opted for a safety pack. Features like lane keep assist and advanced AEB can often lower the car's insurance group rating. For example, a Volkswagen Polo in "Life" trim (Group 3) is often cheaper to insure than a SEAT Ibiza "SE" (Group 11), largely due to the Polo's superior standard safety equipment.

Step 3: Analyse the security suffix

If you're choosing between two identical-looking cars, check their full insurance group code. A car with an "8E" rating will be much cheaper to insure than one with an "8A" or "9D" rating because it exceeds standard security requirements. This is especially important if the car will be parked on a public street rather than a driveway.

Run real quotes on a 3-4 car shortlist

Before buying, build a shortlist of three or four cars and quote each:

- Find the 1-50 or VRR score for each

- Note the security suffix

- Check if it's an automatic or manual

- Run a comparison quote for all four on a single profile. This reveals the cheapest car for your specific teenager.

This removes the guesswork and ensures the final choice reflects the insurer's actual pricing for your child, not the headline group number.

The First Car Guide

Understanding how insurance groups work is only part of the process for finding your teenager's first car. The First Car Guide explains the rest.